India’s paint sector saw recovery return in Q4FY26, although rising raw-material costs are placing margins under pressure. After several quarters of muted demand, the March quarter witnessed a visible improvement in both urban and rural markets, supported by seasonal demand and channel restocking ahead of industry-wide price hikes.

According to Equirus Securities’ review of Q4FY26 results, most leading paint manufacturers reported healthy volume growth during the quarter, while management commentary pointed to improving demand conditions and greater confidence heading into FY27.

However, a sharp increase in raw material costs and multiple rounds of price hikes suggest

that the industry’s next challenge will be protecting margins without affecting consumption.

Q4FY26 Paints Scorecard

Key Trends

#1 Demand Recovery Broadens Beyond Premium Urban Markets

The most significant development during the quarter was the return of strong volume

growth across much of the industry.

Equirus notes that demand was supported by two factors: seasonal improvement in January-February and dealer restocking ahead of announced price hikes. Decorative paints

remained the primary growth driver, with both urban and rural markets contributing to

demand expansion. Rural markets, in particular, outperformed urban centres for several

players.

#2 Inflation Triggers a New Pricing Cycle

After a prolonged period of price reductions and promotional activity, the industry entered

a new pricing cycle.

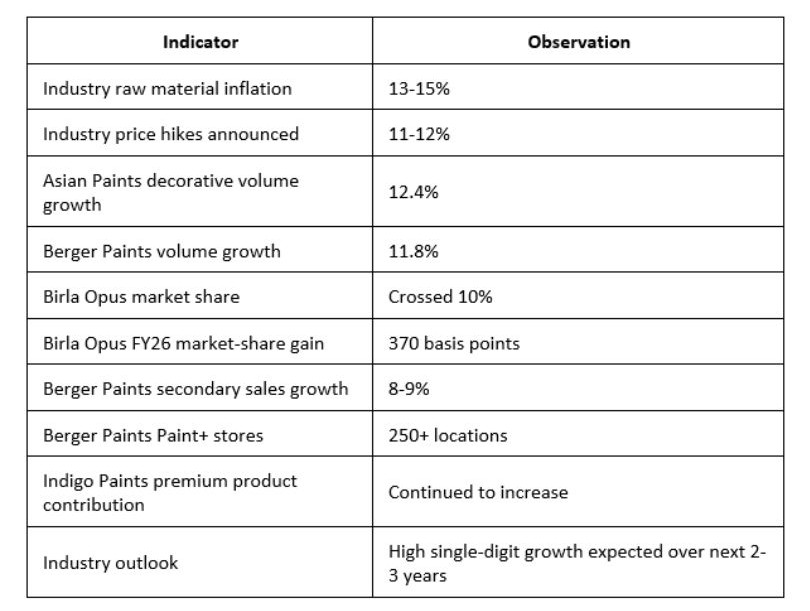

Raw material inflation accelerated sharply from March onwards, prompting paint manufacturers to implement cumulative price hikes of approximately 11-12% across

multiple phases. Industry participants reported blended raw material cost increases of 13-

15%, largely driven by crude-linked inputs and chemicals.

Management teams expect FY27 to witness a reversal of the volume-value gap seen in

recent years, with value growth likely to exceed volume growth as higher prices begin

flowing through the system.

#3 Market Share Battles Give Way to Margin Management

The industry’s competitive intensity remains high, but management commentary suggests

that some of the aggressive pricing strategies employed over the past two years are

beginning to moderate.

Several companies indicated that higher raw material costs have reduced the pricing advantage previously enjoyed by challengers. Promotional schemes and incentives have also begun normalising, creating a more stable operating environment.

#4 Premiumisation Emerges as the Preferred Growth Strategy

Beyond the immediate challenges of inflation and competition, the Q4FY26 results reveal a

longer-term shift in how paint manufacturers are pursuing growth.

Rather than relying solely on volume expansion, leading players are increasingly focusing on premium products, specialised coatings and value-added solutions to improve realisations and strengthen profitability.

The trend reflects a broader change in consumer behaviour. As homeowners increasingly

view paint as a design and lifestyle choice rather than a purely functional purchase, demand is shifting towards premium finishes, specialised textures, waterproofing solutions and products offering superior durability and aesthetics.

For manufacturers, premiumisation offers a way to offset rising raw-material costs while

protecting margins. For dealers and retailers, it creates opportunities to improve

profitability through higher-value product mixes. And for the wider interiors ecosystem, it

signals the growing convergence of paints with design, décor and home-improvement

categories.

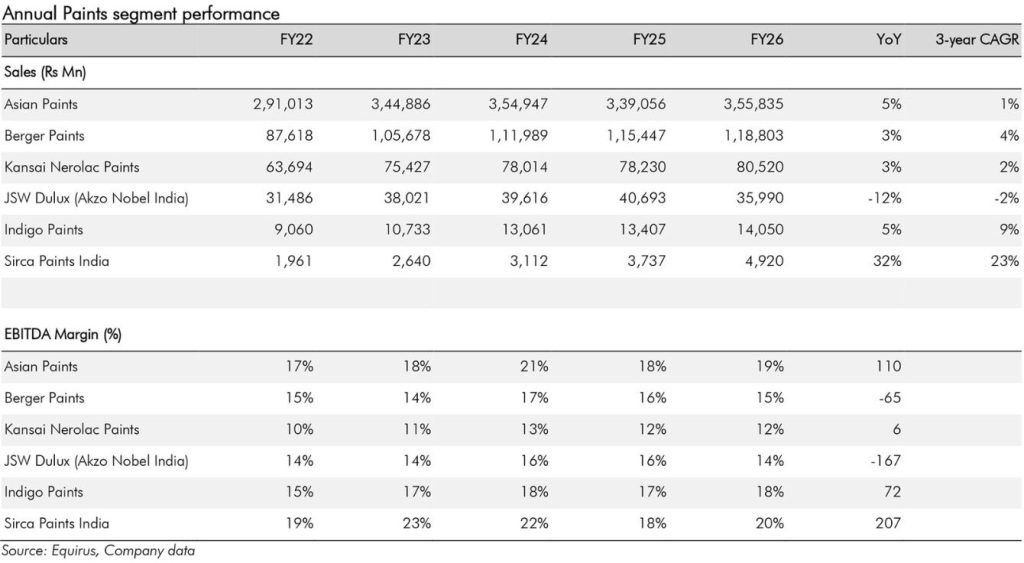

Annual Paints Segment Performance

Why This Matters

- Demand recovery is no longer confined to premium urban markets.

- Price hikes are returning after a prolonged period of discount-led competition.

- Industry growth is shifting from market-share battles to margin management.

- Premiumisation is becoming the industry’s preferred growth and margin lever.

The impact of these trends becomes clearer when viewed through the revenue and

profitability performance of the industry’s leading players.

What the Charts Reveal

Viewed together, the revenue and EBITDA exhibits point to these emerging realities:

- Demand recovery is broad-based

Revenue growth has returned across most major paint companies, indicating that the

recovery is not confined to a handful of markets or brands.

- Business models are diverging

While Asian Paints and Berger Paints continue to leverage scale, premiumisation and

distribution strength, Birla Opus is prioritising market-share expansion. Indigo Paints,

meanwhile, is building a differentiated premium niche.

- Premiumisation is becoming a common strategic theme

Despite differences in scale and market positioning, most leading players are investing in

premium products, specialised coatings and value-added categories. This suggests that

future growth will increasingly be driven by product mix and realisations rather than volume alone.

- Competition is entering a new phase

The focus is gradually shifting from aggressive discounting and market-share battles towards pricing discipline and profitability management as raw-material costs rise.

- FY27 could mark the beginning of a new margin cycle

After benefiting from relatively benign input costs in recent years, manufacturers now face inflation in crude-linked raw materials and chemicals. The ability to preserve EBITDA margins without compromising growth will become a key differentiator.

“Competitive aggression will remain, but intensity should gradually taper

off leading to better volume-value matrix for the industry. Investment in

strengthening Distribution reach along-with cost discipline will remain key

focus areas for the companies.”

— Pranav Mehta, Associate Director, Equirus Securities

Company Strategies: How Market Leaders Are Preparing for FY27

Asian Paints: Defending Leadership Through Premiumisation and Scale

Asian Paints reported decorative volume growth of 12.4% during the quarter, supported by improving demand conditions and dealer stocking activity ahead of price hikes.

The company continues to focus on premiumisation, product innovation and distribution expansion. New products contributed approximately 17% of revenues, underlining the

company’s focus on premiumisation and innovation-led growth, while nearly 4,000 retailers

were added during the year. Management remains confident of sustaining high single-digit

volume growth in FY27 despite increasing competitive intensity.

The revenue and EBITDA trends underscore the benefits of scale. Despite heightened

competition, Asian Paints continues to demonstrate strong pricing power and operational

efficiency. As raw-material inflation returns, investors and industry observers will closely

monitor the company’s ability to protect margins while maintaining growth momentum.

FY27 Focus: Premium products, innovation-led growth and margin protection.

Berger Paints: Building a Broader Home Improvement Portfolio

Berger Paints reported volume growth of 11.8%, supported by healthy demand across

decorative paints, construction chemicals and waterproofing solutions.

The company continues to strengthen its Paint+ retail network, which has now crossed 250

stores, while also expanding its project business and premium product portfolio. Secondary

sales growth of 8-9% indicates that underlying demand remains healthy.

The revenue trend reflects Berger’s success in diversifying beyond conventional decorative

paints. Its increasing exposure to construction chemicals and waterproofing products may

provide additional growth drivers as housing completions accelerate. The key challenge will

be maintaining profitability as inflationary pressures intensify across input materials.

FY27 Focus: Diversification, premiumisation and profitable growth.

Kansai Nerolac: Leveraging Industrial Coatings for Stability

Kansai Nerolac’s performance was driven primarily by industrial coatings, with strong

demand from automotive, infrastructure and manufacturing sectors.

Growth in passenger vehicles, commercial vehicles, SUVs and tractors supported the

company’s industrial business, helping offset relatively softer performance in decorative

paints. This diversified revenue mix provides Kansai Nerolac with a degree of insulation from the intense competition currently affecting the decorative segment.

The company’s revenue and profitability profile remains closely linked to broader

manufacturing activity. While decorative paints remain important, industrial coatings are

likely to remain the primary growth engine in FY27.

FY27 Focus: Industrial coatings growth and manufacturing-led demand.

Birla Opus: The Challenger Reshaping the Industry

No company has altered the competitive landscape more dramatically than Birla Opus.

Management estimates suggest the brand has crossed 10% market share in decorative

paints, gaining approximately 370 basis points during FY26. During the year, the company

launched 42 new products and expanded its portfolio to more than 1,850 SKUs.

Distribution expansion remains a central pillar of its strategy. The company now reaches

over 11,500 towns and aims to expand that footprint to 15,000 towns by the end of FY27.

The rapid expansion has already begun influencing pricing behaviour, dealer engagement

models and competitive strategies across the industry. Its stated ambition is to become

India’s second-largest decorative paints company while targeting revenues of ₹10,000 crore by FY28.

At this stage, revenue growth and market-share acquisition remain more important than

profitability. However, the industry’s next major question will be whether Birla Opus can

sustain rapid expansion while progressively improving margins.

FY27 Focus: Market-share gains, distribution expansion and scale.

Indigo Paints: Winning Through Differentiation

Indigo’s strategy demonstrates that premiumisation is no longer limited to market leaders.

The company is using differentiated products and specialised categories to build pricing

power and improve realisations.

The company has consistently reported value growth ahead of volume growth, reflecting a

deliberate focus on premiumisation. It is also strengthening its presence in Tier 3 and Tier 4 markets while expanding manufacturing capacity through its new facility in Jodhpur.

The company’s revenue trajectory highlights the growing importance of niche positioning

within the paints industry. Rather than competing directly with larger players on scale,

Indigo is building a defensible position through differentiated products and superior

realisations.

Its ability to maintain healthy profitability while continuing to expand distribution will

remain a key area of interest during FY27.

FY27 Focus: Premium niches, differentiated products and regional expansion.

“We believe FY27-29 will be a relatively better growth period versus

FY24-26 for late-stage building materials like paints, as real estate

launches of FY22-25 start reaching the completion stage.”

— Pranav Mehta, Associate Director, Equirus Securities

SH Takeaway

#1 For Contractors

The return of price hikes means project costing assumptions may need revision.

Most major paint manufacturers have already implemented multiple rounds of increases,

and further adjustments cannot be ruled out if raw material inflation persists. Contractors

may increasingly favour brands that offer stable supply and predictable pricing rather than

chasing short-term discounts.

#2 For Retailers and Dealers

The channel benefited from restocking activity during Q4FY26, but growth in FY27 will

depend on genuine consumer demand rather than inventory build-up.

Retailers should monitor the pace of secondary sales closely, particularly during the festive

and post-monsoon periods. Product mix is also becoming increasingly important as

premium categories continue to outperform.

#3 For the Interior Ecosystem

Paints are often among the final categories to benefit from residential construction activity.

The improvement witnessed during Q4FY26 therefore offers an encouraging signal for the

broader interiors market.

As residential projects launched during the 2022-25 period move toward completion and

handover, demand for paints, decorative finishes, furniture, cabinetry, hardware and

interior products could receive a meaningful boost.

In that sense, paints may be acting as a leading indicator for the broader interiors

ecosystem. If demand momentum sustains through FY27, categories such as decorative

surfaces, cabinetry, furniture, hardware and home improvement products could be among

the next beneficiaries.

ALSO READ